The Federal Reserve Bank is not a government institution, it has no reserves, and it is not a bank. It is a cartel that was created in top secrecy and deceptively put into place in 1913. It’s goal is to maintain control in the financial system, and therefore their powerhold by keeping We The People in never-ending debt, aka Debt Slaves. The Fed has followed a consistent policy of flooding the economy with easy money, leading to a misallocation of resources and an artificial “boom” followed by a recession or depression when the Fed-created bubble bursts. From the Great Depression, to the stagflation of the seventies, to the burst of the dotcom bubble, to the housing market crisis, every economic downturn suffered by the country over the last 80 years can be traced to Federal Reserve policy.

In order to understand the Federal Reserve, we must first understand its origins and context. We must deconstruct the puzzle. The first piece of that puzzle lies here, in the White House. This is where the Federal Reserve Act, then known as the Currency Bill, was signed into law after passing the House and Senate in late December, 1913. The New York Times of Christmas Eve, 1913, described the festive scene:

“The Christmas spirit pervaded the gathering. While the ceremony was a little less impressive than that of the signing of the Tarriff act on Oct. 3 last in the same room, the spectators were much more enthusiastic and seized every occasion to applaud.”

There in the White House that fateful December evening, President Wilson signed away the last veneer of control over the American money supply to a cartel; a well-organized gang of crooks so successful, so cunning, so well-hidden that even now, a century later, few know of its existence, let alone the details of its operations. But those details have been openly admitted for decades.

Of course, just as we have been taught to find economics boring, we have been taught that this story is boring. This is the way the Federal Reserve itself tells it:

The United States was facing severe financial problems. At the turn of the century, most banks were issuing their own currency called “bank notes.” The trouble was, currency that was good in one state was sometimes worthless in another. People began to lose confidence in their money, since it was only as sound as the bank that issued it. Fearful that their bank might go out of business, they rushed to exchange their bank notes for gold or silver. By attempting to do so, they created the panic of 1907.

SOURCE: Where The Bankers Bank

During the panic, people streamed to the banks and demanded their deposits. The banks could not meet the demand; they simply did not have enough gold and silver coin available. Many banks went under. People lost millions of dollars, businesses suffered, unemployment rose, and the stability of our economic system was again threatened.

Well, this couldn’t go on. If the country was going to grow and prosper, some means would have to be found to achieve financial and economic stability.

To prevent financial panics like the one in 1907, President Woodrow Wilson signed The Federal Reserve Act into law in 1913.

SOURCE: Too Much, Too Little

But this is history as told by the victors: a revisionist vision in which the creation of a central bank to control the nation’s money supply is merely a boring historical footnote, about as important as the invention of the zipper or an early 20th century hoola-hoop craze. The truth is that the story of the secret banking conclave that gave birth to that Federal Reserve Act is as exciting and dramatic as any Hollywood screenplay or detective novel yarn, and all the more remarkable for the fact that it is all true.

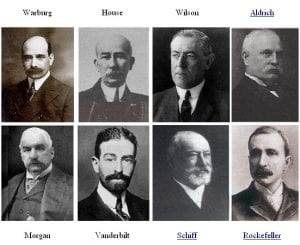

We pick up the story, appropriately enough, under cover of darkness. It was the night of November 22, 1910, and a group of the richest and most powerful men in America were boarding a private rail car at an unassuming railroad station in Hoboken, New Jersey. The car, waiting with shades drawn to keep onlookers from seeing inside, belonged to Senator Nelson Aldrich, the father-in-law of billionaire heir to the Rockefeller dynasty, John D. Rockefeller, Jr. A central figure on the influential Senate Finance Committee where he oversaw the nation’s monetary policy, Aldrich was referred to in the press as the “General Manager of the Nation.” Joining him that evening was his private secretary, Shelton, and a who’s who of the nation’s banking and financial elite: A. Piatt Andrew, the Assistant Treasury Secretary; Frank Vanderlip, President of the National City Bank of New York; Henry P. Davison, a senior partner of J.P. Morgan Company; Benjamin Strong, Jr., an associate of J.P. Morgan and President of Bankers Trust Co., and Paul Warburg, heir of the Warburg banking family and son-in-law of Solomon Loeb of the famed New York investment firm, Kuhn, Loeb & Company.

We pick up the story, appropriately enough, under cover of darkness. It was the night of November 22, 1910, and a group of the richest and most powerful men in America were boarding a private rail car at an unassuming railroad station in Hoboken, New Jersey. The car, waiting with shades drawn to keep onlookers from seeing inside, belonged to Senator Nelson Aldrich, the father-in-law of billionaire heir to the Rockefeller dynasty, John D. Rockefeller, Jr. A central figure on the influential Senate Finance Committee where he oversaw the nation’s monetary policy, Aldrich was referred to in the press as the “General Manager of the Nation.” Joining him that evening was his private secretary, Shelton, and a who’s who of the nation’s banking and financial elite: A. Piatt Andrew, the Assistant Treasury Secretary; Frank Vanderlip, President of the National City Bank of New York; Henry P. Davison, a senior partner of J.P. Morgan Company; Benjamin Strong, Jr., an associate of J.P. Morgan and President of Bankers Trust Co., and Paul Warburg, heir of the Warburg banking family and son-in-law of Solomon Loeb of the famed New York investment firm, Kuhn, Loeb & Company.

The men had been told to arrive one by one after sunset to attract as little attention as possible. Indeed, secrecy was so important to their mission that the group did not use anything but their first names throughout the journey so as to keep their true identities secret even from their own servants and wait staff. The movements of any one of them would have been reason enough to attract the attention of New York’s voracious press, especially in an era where banking and monetary reform was seen as a key issue for the future of the nation; a meeting of all of them, now that would surely have been the story of the century. And it was.

Their destination? The secluded Jekyll Island off the coast of Georgia, home to the prestigious Jekyll Island Club whose members included the Morgans, Rockefellers, Warburgs and Rothschilds. Their purpose? Davison told intrepid local newspaper reporters who had caught wind of the meeting that they were going duck hunting. But in reality, they were going to draft a reform of the nation’s banking industry in complete secrecy.

G. Edward Griffin, the author of the bestselling The Creature from Jekyll Island and a long-time Federal Reserve researcher, explains:

G. Edward Griffin: What happened is the banks decided that since there was going to be legislation anyway to control their industry, that they wouldn’t just sit back and wait and see what happened and cross their fingers that it would be OK. They decided to do what so many cartels do today: they decided to take the lead. And they would be the ones calling for regulations and reform.

They like the word “reform.” The American people are suckers for the word “reform.” You just put that into any corrupt piece of legislation, call it “reform” and people say “Oh, I’m all for ‘reform’,” and so they vote for it or accept it.

So that’s what they were doing. They decided, “We will ‘reform’ our own industry.” In other words, “We will create a cartel and we will give the cartel the power of government. We’ll take our cartel agreement so we can self-regulate to our advantage and we’ll call it ‘The Federal Reserve Act.’ And then we’ll take this cartel agreement to Washington and convince those idiots there to pass it into law.”

And that basically was the strategy. It was a brilliant strategy. Of course we see it happening all the time, certainly in our own day today we see the same thing happened in other cartelized industries. Right now we’re watching it unfold in the field of healthcare, but at that time it was banking, alright?

And so the banking cartel wrote their own rules and regulations, called it “The Federal Reserve Act,” got it passed into law, and it was very much to their liking because they wrote it. And in essence what they had created was a set of rules that made it possible for themselves to regulate their industry, but they went even beyond that. In fact, it’s clear to me when I was reading their letters and their conversation at the time, and the debates, that they never dreamed that Congress would go along and also give them the right to issue the nation’s money supply. Not only were they now going to regulate their own industry, which is what they started out as wanting to do, but they got this incredible gift that they didn’t dream would be given to them (although they were negotiating for it), and that was that Congress gave them the authority to issue the nation’s money. Congress gave away the sovereign right to issue the nation’s money to the private banks.

And so all of this was in The Federal Reserve Act, and the American people were joyous because they were told, and they were convinced, that this was finally a means of controlling this big creature from Jekyll Island.

SOURCE: Interview with G. Edward Griffin

Amazingly enough, they were successful, not just in conspiring to write the legislation that would eventually become the Federal Reserve Act, but in keeping that conspiracy a secret from the public for decades. It was first reported on in 1916 by Bertie Charles Forbes, the financial writer who would later go on to found Forbes magazine, but it was never fully admitted until a full quarter century later when Frank Vanderlip wrote a casual admission of the meeting in the February 9, 1935 edition of The Saturday Evening Post:

“I was as secretive—indeed, as furtive—as any conspirator.[…]I do not feel it is any exaggeration to speak of our secret expedition to Jekyll Island as the occasion of the actual conception of what eventually became the Federal Reserve System.”

Over the course of their nine days of deliberation at the Jekyll Island club, they devised a plan so overarching, so ambitious, that even they could scarcely imagine that it would ever be passed by congress. As Vanderlip put it,

“Discovery [of our plan], we knew, simply must not happen, or else all our time and effort would be wasted. If it were to be exposed publicly that our particular group had got together and written a banking bill, that bill would have no chance whatever of passage by Congress.”

So what, precisely, did this conclave of conspirators devise at their Jekyll Island meeting? A plan for a central banking system to be owned by the banks themselves, a system which would organize the nation’s banks into a private cartel that would have sole control over the money supply itself. At the end of their nine day meeting, the bankers and financiers went back to their respective offices content in what they had accomplished. The details of the plan changed between its 1910 drafting and the eventual passage of the Federal Reserve Act, but the essential ideas were there.

But ultimately, this scene on Jekyll Island, too, is just one piece of a larger puzzle. And like any other puzzle piece, it has to be seen in its wider context for the bigger picture to become visible. To understand the other pieces of the puzzle and their importance in the creation of the Federal Reserve, we have to travel backward in time.

The story begins in late 17th century Europe. The Nine Years’ War is raging across the continent as Louis XIV of France finds himself pitted against much of the rest of the continent over his territorial and dynastic claims. King William III of England, devastated by a stunning naval defeat, commits his court to rebuilding the English navy. There’s only one problem: money. The government’s coffers have been exhausted by the waging of the war and William’s credit is drying up.

A Scottish banker, William Paterson, has a banker’s solution: a proposal “to form a company to lend a million pounds to the Government at six percent (plus 5,000 “management fee”) with the right of note issue.” By 1694 the idea has been slightly revised (a 1.2 million pound loan at 8 percent plus 4000 for management expenses), but it goes ahead: the magnanimously titled Bank of England is created.

The name is a carefully constructed lie, designed to make the bank appear to be a government entity. But it is not. It is a private bank owned by private shareholders for their private profit with a charter from the king that allows them to print the public’s money out of thin air and lend it to the crown. What happens here at the birth of the Bank of England in 1694 is the creation of a template that will be repeated in country after country around the world: a privately controlled central bank lending money to the government at interest, money that it prints out of nothing. And the jewel in the crown for the international bankers that creates this system is the future economic powerhouse of the world, the United States.

In many important respects, the history of the United States is the history of the struggle of the American people against the bankers that wish to control their money. By the 1780s, with colonies still fighting for independence from the crown, the bankers will get their wish.

In 1781 the United States is in financial turmoil. The Continental, the paper currency issued by the Continental Congress to pay for the war, has collapsed from overissue and British counterfeiting. Desperate to find a way to finance the end stages of the war, Congress turns to Robert Morris, a wealthy shipping merchant who was investigated for war profiteering just two years earlier. Now as “Superintendent of Finance” of the United States from 1781 to 1784 he is regarded as the most powerful man in America next to General Washington.

In his capacity as Superintendent of Finance, Morris argues for the creation of a privately-owned central bank deliberately modeled on the Bank of England that the colonies were supposedly fighting against. Congress, backed into a corner by war obligations and forced to do business with the bankers just like King William in the 1690s, acquiesces and charters the Bank of North America as the nation’s first central bank. And exactly as the Bank of England came into existence loaning the British crown 1.2 million pounds, the B.N.A. started business by loaning $1.2 million to Congress.

By the end of the war, Morris has fallen out of political favor and the Bank of North America’s currency has failed to win over a skeptical public. The B.N.A. is downgraded from a national central bank to a private commercial bank chartered by the State of Pennsylvania.

But the bankers have not given up yet. Before the ink is even dry on the constitution, a group led by Alexander Hamilton is already working on the next privately-owned central bank for the newly formed United States of America.

So brazen is Hamilton in the forwarding of this agenda that he makes no attempt to hide his aims or those of the banking interests he serves:

“A national debt, if it is not excessive, will be to us a national blessing,” he wrote in a letter to James Duane in 1781. “It will be a powerful cement of our Union. It will also create a necessity for keeping up taxation to a degree which, without being oppressive, will be a spur to industry.”

Opposition to Hamilton and his debt-based system for establishing the finances of the US is fierce. Led by Jefferson and Madison, the bankers and their system of debt-enslavement is called out for the force of destruction that it is. As Thomas Jefferson wrote:

“[T]he spirit of war and indictment, […] since the modern theory of the perpetuation of debt, has drenched the earth with blood, and crushed its inhabitants under burdens ever accumulating.”

Still, Hamilton proves victorious. The First Bank of the United States is chartered in 1791 and follows the pattern of the Bank of England and the Bank of North America almost exactly; a privately-owned central bank with the authority to loan money that it creates out of nothing to the government. In fact, it is the very same people behind the new bank as were behind the old Bank of North America. It was Alexander Hamilton, Robert Morris’ former aide, who first proposed Morris for the position of Financial Superintendent, and the director of the old Bank of North America, Thomas Willing, is brought in to serve as the first director of the First Bank of the United States. Meet the new banking bosses, same as the old banking bosses.

In the first five years of the banks’ existence, the US government borrows 8.2 million dollars from the bank and prices rise 72%. By 1795, when Hamilton leaves office, the incoming Treasury Secretary announces that the government needs even more money and sells off the government’s meager 20% share in the bank, making it a fully private corporation. Once again, the US economy is plundered while the private banking cartel laughs all the way to the bank that they created.

By the time the bank’s charter comes due for renewal in 1811, the tide has changed for the money interests behind the bank. Hamilton is dead, shot to death in a duel with Aaron Burr. The bank-supporting Federalist party is out of power. The public are wary of foreign ownership of the central bank, and what’s more don’t see the point of a central bank in time of peace. Accordingly, the charter renewal is voted down in the Senate and the bank is closed in 1811.

Less than a year later, the US is once again at war with England. After 2 years of bitter struggle the public debt of the US has nearly tripled from $45.2 million to $119.2 million. With trade at a standstill, prices soaring, inflation rising and debt mounting, President Madison signs the charter for the creation of another central bank, the Second Bank of the United States, in 1816. Just like the two central banks before it, it is majority privately-owned and is granted the power to loan money that it creates out of thin air to the government.

The 20 year bank charter is due to expire in 1836, but President Jackson has already vowed to let it die prior to renewal. Believing that Jackson won’t risk his chance for reelection in 1832 on the issue, the bankers forward a bill to renew the bank’s charter in July of that year, 4 years ahead of schedule. Remarkably, Jackson vetoes the renewal charter and stakes his reelection on the people’s support of his move. In his veto message, Jackson writes in no uncertain terms about his opposition to the bank:

“Whatever interest or influence, whether public or private, has given birth to this act, it can not be found either in the wishes or necessities of the executive department, by which present action is deemed premature, and the powers conferred upon its agent not only unnecessary, but dangerous to the Government and country. It is to be regretted that the rich and powerful too often bend the acts of government to their selfish purposes.[…]If we can not at once, in justice to interests vested under improvident legislation, make our Government what it ought to be, we can at least take a stand against all new grants of monopolies and exclusive privileges, against any prostitution of our Government to the advancement of the few at the expense of the many, and in favor of compromise and gradual reform in our code of laws and system of political economy.”

The people side with Jackson and he’s reelected on the back of his slogan, “Jackson and No Bank!” The President makes good on his pledge. In 1833 he announces that the government will stop using the bank and will pay off its debt. The bankers retaliate in 1834 by staging a financial crisis and attempting to pin the blame on Jackson, but it’s no use. On January 8, 1835, President Jackson succeeds in paying off the debt, and for the first and only time in its history the United States is free from the debt chain of the bankers. In 1836 the Second Bank of the United States’ charter expires and the bank loses its status as America’s central bank.

It is 77 years before the bankers can regain the jewel in their crown. But it is not for lack of trying. Immediately upon the death of the bank, the banking oligarchs in England react by contracting trade, removing capital from the U.S., demanding payment in hard currency for all exports, and tightening credit. This results in a financial crisis known as the Panic of 1837, and once again Jackson’s campaign to kill the bank is blamed for the crisis.

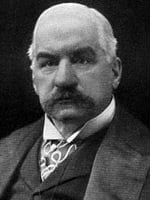

Throughout the late 19th century the United States is rocked by banking panics brought about by wild banking speculation and sharp contractions in credit. By the dawn of the 20th century, the bulk of the money in the American economy has been centralized in the hands of a small clique of industrial magnates, each with a near monopoly on a sector of the economy. There are the Astors in real estate, the Carnegies and the Schwabs in steel, the Harrimans, Stanfords and Vanderbilts in railroads, the Mellons and the Rockefellers in oil. As all of these families start to consolidate their fortunes, they gravitate naturally to the banking sector. And in this capacity, they form a network of financial interests and institutions that centered largely around one man, banking scion and increasingly America’s informal central banker in the absence of a central bank, John Pierpont Morgan.

John Pierpont Morgan, or “Pierpont” as he prefers to be called, is born in Hartford, Connecticut in 1837 to Junius Spencer Morgan, a successful banker and financier. Morgan rides his father’s coattails into the banking business and by 1871 is partnered in his own firm, the firm that was eventually to become J.P. Morgan and Company.

It is Morgan who finances Cornelius Vanderbilt’s New York Central Railroad. It is Morgan that finances the launch of nearly every major corporation of the period, from AT&T to General Electric to General Motors to Dupont. It is Morgan who buys out Carnegie and creates the United States Steel Corporation, America’s first billion dollar company. It is Morgan who brokers a deal with President Grover Cleveland to “save” the nation’s gold reserves by selling 62 million dollars worth of gold to the Treasury in return for government bonds. And it is Morgan, who, in 1907, sets in motion the crisis that leads to the creation of the Federal Reserve.

That year, Morgan begins spreading rumors about the precarious finances of the Knickerbocker Trust Company, a Morgan competitor and one of the largest financial institutions in the United States at the time. The resulting crisis, dubbed the Panic of 1907, shakes the U.S. financial system to its core. Morgan puts himself forward as a hero, boldly offering to help underwrite some of the faltering banks and brokerage houses to keep them from going under. After a bout of hand-wringing over the nation’s finances, a Congressional Committee is assembled to investigate the “money trust,” the bankers and financiers who brought the nation so close to financial ruin and that wield such power over the nation’s finances. The public follows the issue closely, and in the end a handful of bankers are identified as key players in the money trust’s operations, including Paul Warburg, Benjamin Strong, Jr., and J.P. Morgan.

Andrew Gavin Marshall, editor of The People’s Book Project, explains:

Andrew Gavin Marshall: At the beginning of the 20th century there was an investigation following the greatest of these financial panics, which was in 1907, and this investigation was on “the money trust.” It found that three banking interests–J.P. Morgan, National City Bank, and the City Bank of New York–basically controlled the entire financial system. Three banks. The public hatred toward these institutions was unprecedented. There was an overwhelming consensus in the country for establishing a central bank, but there were many different interests in pushing this and everyone had their own purpose behind advocating for a central bank.

So to represent most people, you had farmer interests, populists, progressives, who were advocating a central bank because they couldn’t take the recurring panics, but they wanted government control of the central bank. They wanted it to be exclusively under the public control because they despised and feared the New York banks as wielding too much influence, so for them a central bank would be a way to curb the power of these private financial interests.

On the other hand, those same financial interests were advocating for a central bank to serve as a source of stability for their control of the system, and also to act as a lender of last resort to them so they would never have to face collapse. But also, in order to exert more control through a central bank, the private New York banking community wanted a central bank under the exclusive control of them. There’s a shocker.

So you had all these various interests which converged. Of course, the most influential happened to be the New York financial houses which were more aligned with the European financial houses than they were with any other element in American society. The main individual behind the founding of the Federal Reserve was Paul Warburg, who was a partner with Kuhn, Loeb and Company, a European banking house. His brothers were prominent bankers in Germany at that time, and he had of course close connections with every major financial and industrial firm in the United States and most of those existing in Europe. And he was discussing all of these ideas with his fellow compatriots in advocating for a central bank. In 1910, Warburg got the support of a Senator named Nelson Aldrich, whose family later married into the Rockefeller family (again, I’m sure just a coincidence). Aldrich invited Warburg and a number of other bankers to a private, secret meeting on Jekyll Island just off the coast of Georgia where they met in 1910 to discuss the construction of a central bank in the United States, but one which would of course be owned by and serve the interests of the private bank. Aldrich then presented this in 1911 as the “Aldrich Plan” in the U.S. Congress, but it was actually voted out.

The public, suspicious of Senator Aldrich’s banking connections, ultimately reject the Jekyll Island cabal’s “Aldrich Plan.” The cabal does not give up, however. They simply revise and rename their plan, giving it a new public face, that of Representative Carter Glass and Senator Robert Owen.

In the end, the money trust that was behind the Panic of 1907 uses the public’s own outrage against them to complete their consolidation of control over the banking system. The newly-retitled Federal Reserve Act is signed into law on December 23, 1913 and the Fed begins operations the next year.

Continued on next page…